Financial Wizardry or Blood Magic?

Financial Wizardry or Blood Magic?

A Sustainability Analysis of the Systemic Value Flows Behind Abracadabra.Money

Disclaimer: This article is meant to be seen as a case study of an existing protocol’s mechanics. This article is not meant to be used or construed as financial advice, and it may contain false information and/or omit critical information. I may have a financial stake in any of the assets or protocols described and therefore may also be biased. There is a large amount of risk inherent to using or investing in anything within the DeFi and cryptocurrency industry. Please do your own research and come to your own independent conclusions before making any financial decisions.

Editor’s note on September 27th, 2021: A lot of time has passed since the original posting of this on June 29th, and therefore a lot of circumstances have changed that I am no longer keeping track of. If you are reading this article now, please do not assume that these mechanics are still as described here. However, this post is still a key demo of an approach to breaking down tokenomics and system design. I hope you learn something new!

Preface

Our first project-focused exploration into the galaxy of DeFi will not be for the faint of heart. This article is very technical and dense in nature. In an attempt to prevent you from getting lost in the ambiguity, this guide contains an intense amount of detail. In preparation for imminent liftoff, I suggest you grab a cup of coffee, sit down, and prepare for a long ride! :)

Table of Contents

A Magical $SPELL

A brief introduction to Abracadabra for those unfamiliar

The Mechanics of Spellcasting

An introduction to how the core Abracadabra system functions from varying perspectives

Guild Dynamics

Generally identifying the incentives around how each party interacts with each other within the system

Misdirection

Critically analyzing where the values flow in and out of the system

Glimmer of Hope

An optimistic outlook on how Abracadabra could be sustainable

Studies of Magical Stability

Some separate observations of similar systems and how they relate

Advanced Transfiguration

A conclusion to the drawn out observations and overall analysis of Abracadabra

A Magical $SPELL

Our first journey takes us to a planet that exists on the edge of the Lending and Stablecoin sectors of the DeFi galaxy. Its residents have recently adopted a new magical system and founded a new protocol called Abracadabra.

Abracadabra.Money has recently launched their protocol designed to allow users to collateralize their interest-bearing tokens (ibTokens) and borrow against them. This system introduces two new primary tokens:

$MIM — A stablecoin mintable by the protocol, each designed to represent $1 USD (Chainlink price oracle) of the collateralized ibTokens that are being borrowed against.

$SPELL — The governance token of the Abracadabra ecosystem. It also is used as the primary liquidity mining subsidy within the system.

The overall concept is a useful tool for DeFi participants to achieve more fluid means of collateralization, but let’s look deeper into how the value flows throughout the entire Abracadabra system. As a third party, we may be able to identify the critical strengths and weaknesses inherent to the design.

The Mechanics of Spellcasting

First, let’s outline how the protocol operates on a base level. If you already know how Abracadabra works, you can skip forward to Guild Dynamics.

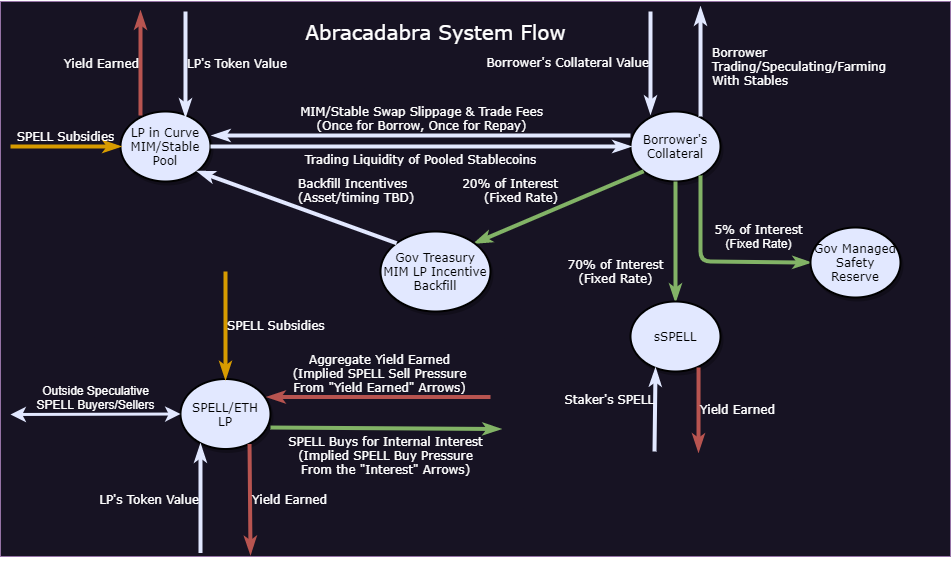

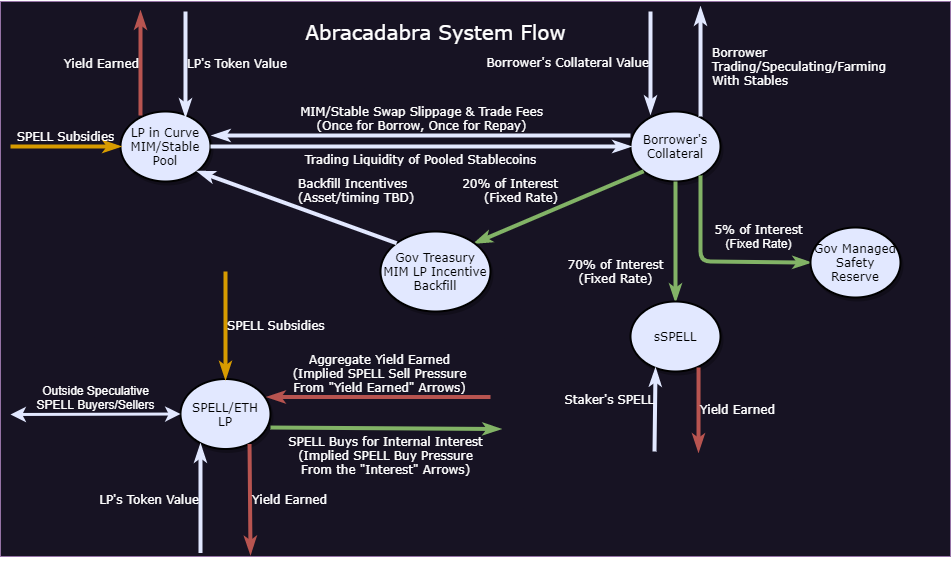

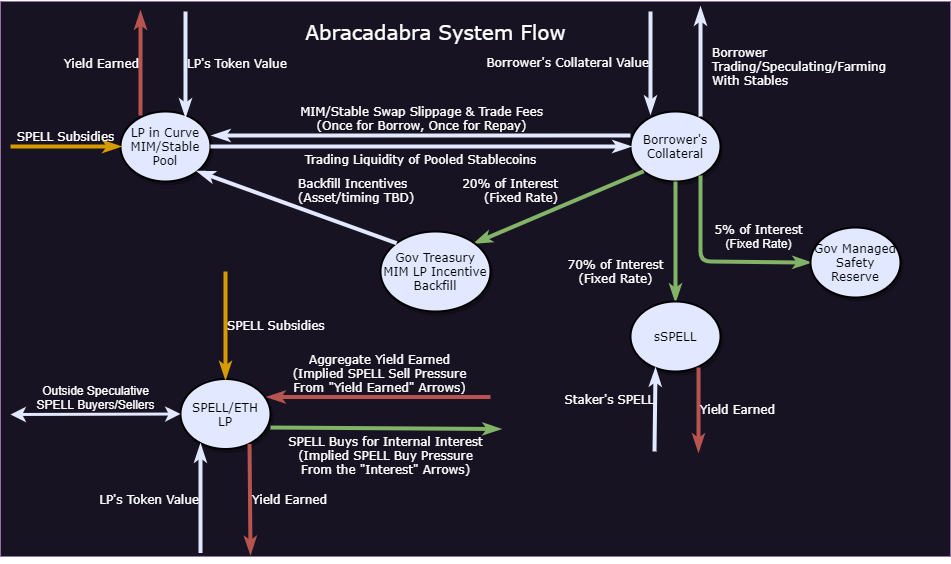

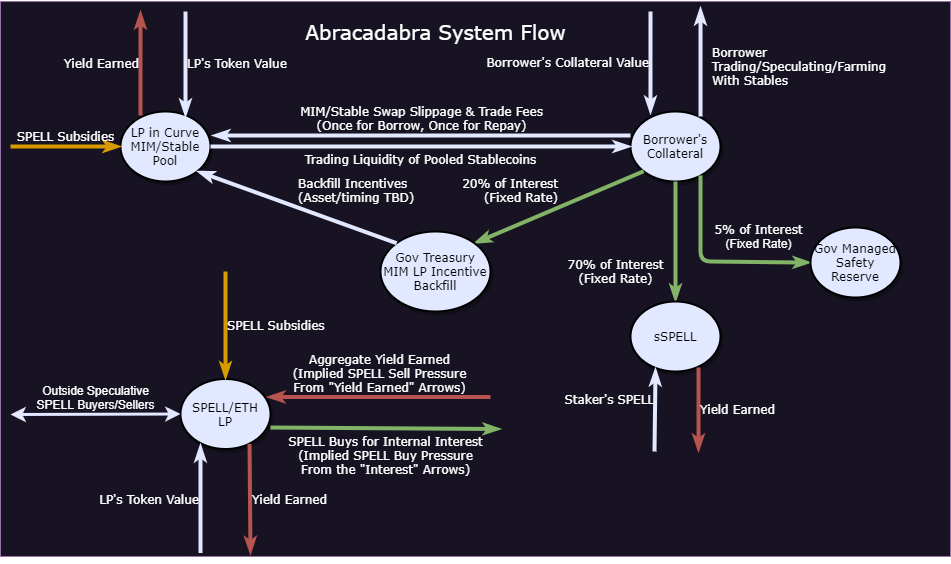

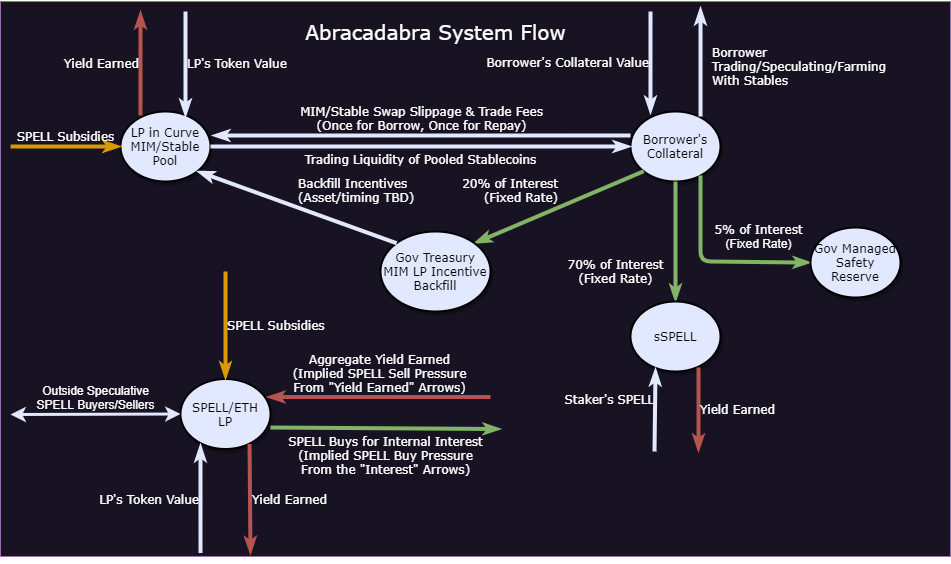

As seen in the diagram above, the system of value flow within Abracadabra is fairly complex. To break down the system, let’s walk through a few different paths from different perspectives.

Borrowers

First, let’s walk through the steps from a Borrower’s perspective:

Borrower deposits qualified ibToken collateral

Borrower mints $MIM to represent their borrowed value at a fixed interest rate determined by the asset collateral parameters

Liquidation parameters also determined by asset, and they assume 1 $MIM = 1 USD (USD Chainlink price oracle)

Borrower trades $MIM for other, more universally accepted stablecoins via the Curve $MIM/Stablecoin pool

Relies on the Curve pool being liquid enough to support the trade

Borrower uses stablecoins as desired throughout DeFi, monitors Abracadabra liquidation risk

To prepare to repay the loan, the Borrower swaps stablecoins for $MIM

Relies on the Curve pool still being liquid enough to support the trade

In order to not incur excess unforeseen fees/loss, the borrower relies on the $MIM/Stablecoin price to be roughly equivalent or cheaper than before when swapping from $MIM to stablecoin

Borrower returns $MIM debt + interest from minting in step 2.

From the borrower’s perspective, this system works great as long as the Curve pool keeps $MIM stable/pegged and liquid. Yes, there is an excess transitory fee incurred when swapping that should be taken into account.

Borrower’s General Exchange of Value:

Pay interest for access to fluid collateralization/borrowing

Borrower’s Benefits:

Stable, relatively low interest rate

Fluid borrowing power while keeping primary ibToken exposure

Borrower’s Concerns:

Liquidation due to collateral value decreasing

$MIM Curve Pool remaining liquid

$MIM remaining at peg (or at least cheaper when buying back $MIM)

Systemic exploit/rug that results in collateral loss (although loss is limited to the spread between collateral value and borrowed value)

Curve Liquidity Providers (MIM-3CRV LPs)

It’s pretty clear that a large portion of the Borrower’s concerns involve the Curve pool & $MIM pricing, so let’s investigate how the Curve LPs are incentivized to participate.

Curve LP deposits a qualified stablecoin ($DAI, $USDC, $USDT, $MIM) and receives MIM-3LP3CRV-f LP token (henceforth referred to as MIM-3CRV)1

Depositor can technically receive more or less MIM-3CRV tokens depending on the balance skew of each token in the pool

Relies on $MIM not experiencing infinite mint exploit

Exposed to losses when exiting and any token in the pool being off-peg

MIM-3CRV LP stakes MIM-3CRV into Abracadabra to receive $SPELL subsidies from the farming/liquidity mining program

At any time, the MIM-3CRV LP can choose to unstake and remove liquidity into a stablecoin of choice

At any time, the MIM-3CRV LP can choose to receive their yield to sell, stake, or Pool2 LP (but remember, they never bought $SPELL, so this is inflationary/implied sell pressure)

Note that the token balances in the pool are critical to pay attention to. If any one of them skews, so does both the individual stablecoin’s price and the price of the MIM-3CRV pool share tokens.

MIM-3CRV LP’s General Exchange of Value:

Provide stablecoin liquidity in exchange for $SPELL yield

MIM-3CRV LP’s Benefits:

Trade Fee Extraction

High $SPELL APY

MIM-3CRV LP’s Concerns:

$MIM infinite mint exploit draining all MIM-3CRV LP value

Stablecoin token balance skew when entering/exiting

Opportunity cost of not farming yield at other protocols with potentially higher rates

Systemic exploit/rug

This last MIM-3CRV LP concern is critical, as stablecoin LPs are generally thought of as mercenaries of yield. If they can find a better perceived risk/reward in some other protocol’s yield, they will almost certainly migrate there.

Interest Flows

The fixed interest extracted from Borrowers floats in a few different directions.

70% of the interest is used to buy back $SPELL and distribute to $sSPELL holders (more on them in the next section)

20% of the interest is used as backfill incentives held in the treasury and managed by governance

The timing and asset type for these incentives appear TBD by governance in a future proposal2

5% of the interest goes to the DAO managed safety fund3

$sSPELL Holders (or $SPELL Stakers)

Finally, we look at those with speculative interest in Abracadabra’s governance token $SPELL. First, let’s look at those who are staking their $SPELL to extract fees from the protocol:

Staker stakes $SPELL (acquired from market buying or yield farming) and receives $sSPELL

Staker’s $sSPELL accumulates more underlying $SPELL through interest extraction from borrowers

At any time, the staker can unstake and sell some or all $SPELL

Staker’s General Exchange of Value:

Stakes $SPELL (no known benefit to system4) and receives more underlying $SPELL

Staker’s Benefits:

Earns $SPELL farm APY

Exposed 100% to $SPELL price action

Staker’s Concerns:

$SPELL downwards price action

High $SPELL inflation (really just leads to downwards price action)

Watching for better risk/reward $SPELL yields elsewhere

Systemic exploit/rug

$SPELL/$ETH LP (Pool2 LP)

I think most members of the DeFi community know the ropes with a Pool2 role.

Pool2 LP deposits $SPELL and $ETH into the $SPELL/$ETH Sushiswap liquidity pool, in equal parts (or zaps either asset) and receives $SPELL/$ETH Sushiswap pool tokens

Pool2 LP stakes Sushiswap pool token in Abracadabra to receive $SPELL subsidies from the farming/liquidity mining program

At any time, the Pool2 LP can choose to unstake, remove liquidity, and sell

At any time, the Pool2 LP can choose to receive their yield to sell, stake, or LP (but remember, they never bought $SPELL, so this is inflationary/implied sell pressure)

Pool2 LP’s General Exchange of Value:

Provide $SPELL/$ETH liquidity in exchange for $SPELL yield, the counterparty to all trades

Pool2 LP’s Benefits:

Earns $SPELL farm APY

Earns trade fees inside the $SPELL/$ETH pool

Exposed 50/50 to $SPELL/$ETH

Pool2 LP’s Concerns:

$SPELL downwards price action (also $ETH downwards price action, but generally speaking most don’t worry too much about that relative to other concerns)

High $SPELL inflation (really just leads to downwards $SPELL price action)

Watching for better risk/reward $SPELL yields elsewhere

Systemic exploit/rug

Guild Dynamics

Now that the magical mechanics of Abracadabra have been defined, let’s observe how each of the wizarding guilds dynamically interact with one another. As you continue reading, you’ll make note that this project relies a lot on its $MIM stablecoin to keep everything operating smoothly.

The Fundamental $MIM Charm

At the current moment of publishing and implementation5, I know of no real place for minted $MIM to go besides the MIM-3CRV pool — through trading and LP deposits. But for the system to remain healthy, the $MIM balance can’t skew too much away from the other stables and depeg (in this case, under $1). Therefore, other non-MIM stablecoins need to be incentivized to be deposited there to support the MIM price. This is where the $SPELL liquidity mining/yield farming for MIM-3CRV pool comes in to fill the gap.

There are still some underlying dynamics that could help support the $MIM price, mainly that those with outstanding $MIM debt have an opportunity to repay the debt at a discount whenever $MIM is under $1. However, it may a spread much larger than just a tiny depeg in order to properly incentivize them to repay the debt. After all, those borrowers may be sitting in crucial leveraged positions elsewhere and not want to give up their positioned opportunities! In the interim, this isn’t really conducive to those who want to open new debt positions but notice that they’re having to pay an excess tax in order to convert from $MIM to a more widely accepted stablecoin.

Liquidity Sorcerers Have No Allegiance

The lesson learned time and time again in DeFi is that farming liquidity usually has little allegiance. Farmers will freely flow to wherever they see the best risk/reward ratio for their favored position. Abracadabra is no exception, and I have just laid out all of the incentives for why one would act/participate in any one of the roles.

What gets really interesting is this dynamic plays a role even internal to the Abracadabra protocol. Generally speaking, there are two different sets of conflicting yields internal to Abracadabra’s system:

MIM-3CRV LPs vs Stablecoin ibToken borrowers (Stablecoin Sorcery)

$sSPELL holders vs Pool2 LPs ($SPELLcasting Sorcery)

Stablecoin Sorcery

In this dueling match, the Stablecoin ibToken borrowers (henceforth known as sBorrowers for short) have a significant advantage over the MIM-3CRV LPs, even though they both fundamentally practice stablecoin magic. The reasons are threefold:

sBorrowers simply source yield from a much more stable, outside realm (yTokens that dip into all of interoperable DeFi allow for more yield depth)

sBorrowers have the optional ability to mimic the magic that the MIM-3CRV LPs can perform (deposit MIM into MIM-3CRV pool and receive stacked yield there as well)

sBorrowers can multitask their spellcasting yield — source yield from their original principal while also conjuring up extra liquidity they can use how they wish (earn base yield from ibToken, and use borrowed assets as desired to earn elsewhere)

Because of unique yield opportunities above that sBorrowers have, MIM-3CRV LPs are constantly tempted to convert to the sBorrowers. In order to keep the yield duel balanced and prevent a significant conversion rate, the MIM-3CRV LPs require a subsidized yield amount significantly above the yield that sBorrowers can source from their principal in other realms.

$SPELLcasting Sorcery

The matchup between the $sSPELL holders and the Pool2 LPs is a duel based a little more on risk/exposure preference, but is at higher stakes.

sSPELL holders’ principal is solely exposed to the value of $SPELL, and their yield is solely exposed to the interest the borrowers are paying out to them. When there is a lot of borrowing, their yields are high and vice versa.

Pool2 LPs’ principal is exposed to both $SPELL and $ETH, but the magnitude of each is half. Their yields come from the system subsidizing $SPELL to them. A little also comes from the trade fees. When $SPELL value is decreasing, they technically have an advantage of losing less principal than the $sSPELL holders. However, the Pool2 LPs may just flee altogether out of fear.

Therefore within this subsystem, Pool2 LPs typically require more yield subsidies than the interest yield harvested by the $sSPELL holders. If borrowing goes up, interest to $sSPELL holders goes up, and yield to Pool2 LPs has to be increased (hopefully by $SPELL value increases, reluctantly by higher token subsidies).

Misdirection

Looking at the core flows of value within the system, we tend to notice that a lot of the system circles around the price of $SPELL. As the price of $SPELL fluctuates, so does the APY. Because of this, it’s critical to look at what the key internal sources of buying pressure and selling pressure are that affect $SPELL’s price.

As shown by the green arrows in the system, interest payments are generally what cause internal buying pressure within the system. External buying pressure can come from outside speculative parties market buying.

As shown by the red arrows in the system, yield in the form of $SPELL (coming from $SPELL subsidies in orange/yellow) is what causes selling pressure within the system. This could technically be delayed — it depends on which farmers employ the “farm and dump” strategy, and which choose to hold on longer. But don’t forget — the yield that the two LP parties are receiving never directly caused buying pressure and still cause selling pressure at some point. External selling pressure can obviously also come from the outside speculative parties that originally market bought and are now market selling.

But where exactly does the value from subsidization come from to prop the system up? What’s the balance between the internal sources of buying and selling pressure?

Blood Magic?

There’s a lot of sensitivities within this complex system that rely on yields being balanced and incentivized at the right time and in the right amount. $SPELL subsidies to MIM-3CRV and Pool2 LPs are critical to maintain liquidity and stability.

It’s also clear from The Fundamental $MIM Charm + Stablecoin Sorcery sections that the yields of the MIM-3CRV pool alone have to be substantially large in order to secure the core functionality of the system. And since $MIM currently has no major place to go but in the MIM-3CRV pool6, each $MIM minted demands stablecoins to support the peg, which those stablecoins demand yield APY.

The amount of interest inflowing per $MIM is already defined from the table below, and is fixed (unless governance changes the values). As we can see from the table below, the interest rates are extremely low. Great for borrowers, but intuition from plenty of other yield farms indicates that the yield APYs must be significantly larger than 1.5%.

In fact, it seems clear that just the points made in Stablecoin Sorcery alone indicate that participants with stablecoins are incentivized to be sBorrowers rather than MIM-3CRV LPs due to the combination of rock bottom borrow interest rates, yield on principal, and ability to borrow liquidity against it to do it all over. The only thing barring them is the “Initial Max” limits.

Even with the “Initial Max” limits, it’s clear that there is a deficit between the systematic income from borrower’s interest and the systematic subsidies of $SPELL into the MIM-3CRV LP and Pool2 LP. Worse yet, 70% of the interest is just being distributed to $sSPELL holders for being there. (Yes, it’s still buying pressure of $SPELL initially, but it can just get turned around and sold at any time — all while the $sSPELL holders aren’t providing any real systemic benefit.) A gaping systematic deficit if I’ve ever seen one.

So what happens from here if this system remains the same? One of two outcomes:

System performs blood magic by slowly bleeding all $SPELL holders & Pool2 LPs dry through inflation outpacing returns (the deficit is made up for through inflation, but this damages $SPELL holders greatly)

System participants descend into madness from performing magic as $MIM depegs and the system starts to break. Borrowers potentially experience larger & unpredictable fees from depeg spread, MIM-3CRV LPs experience massive ‘impermanent’ loss (probably permanent here), etc. TL;DR: Chaos magic

The “blood magic” outcome seems much more likely if the system were to remain the same, but eventually there will be no one left to support the price as the $SPELL liquidity dries up from lost faith.

Glimmer of Hope

This doom-and-gloom conclusion could be invalidated if a few things change. As you have likely taken note, I’ve made sure to add conditions like “if the system remains the same” earlier to make this clear. Here are some things that would certainly help the system become more sustainable (but not guarantee it yet — situationally dependent):

Increase the fixed borrower interest rate & potentially adjust distribution of interest

$MIM gets real adoption as a stablecoin and is used outside of the Abracadabra ecosystem

The Abracadabra system gets restructured in a new, more sustainable fashion

Borrowing interest rate increases could be a quick fix to make the system more sustainable, but may also ostracize borrowers and decrease volume. After some point, borrowers are no longer going to want to participate at such high interest rates. Adjusting the distribution of interest towards the LPs more rather than the $sSPELL holders would aid in this case. A mixture of the two solutions would seem like the most likely sustainable outcome vs just one or the other.

If $MIM garners real usecase adoption, suddenly not all $MIM needs to go to the MIM-3CRV pool. This significantly relieves the pressure on the MIM-3CRV pool stablecoins, and may reduce some of the necessary subsidies. While writing this article, a new proposal was recently made that could drive real $MIM adoption within the Sushiswap ecosystem. Outside adoption alone still doesn’t guarantee sustainability, but it certainly helps. The proposal appears to be a step in the right direction. (I encourage you to research that proposal and come to your own conclusions.)

I’ve also recently caught wind of a $FTM-$MIM incentivized LP on SpookySwap. This may provide some temporary pressure relief on the amount of $MIM in the MIM-3CRV pool. However, if/when the SpookySwap $BOO incentives turn off, a lot of that pressure may likely flow back into the MIM-3CRV pool.

Finally, the Abracadabra system could get restructured in some brand new, sustainable way. It’s hard as a writer to analyze something that doesn’t yet exist, so I’ll cut back on the handwaving. However, there are some other models out there that could prove sustainable.

Studies of Magical Stability

For the sake of study, there could be more efficient & effective models out there that could achieve the same function of allowing users to borrow against their ibTokens. The following models aren’t necessarily meant as suggestions to Abracadabra — as the models would cut out $SPELL from the core system. I also won’t go quite as deep into the details; at this point I’m sure most of the readers have already thrown in the towel from my long-windedness and tendencies for detail & nuance.

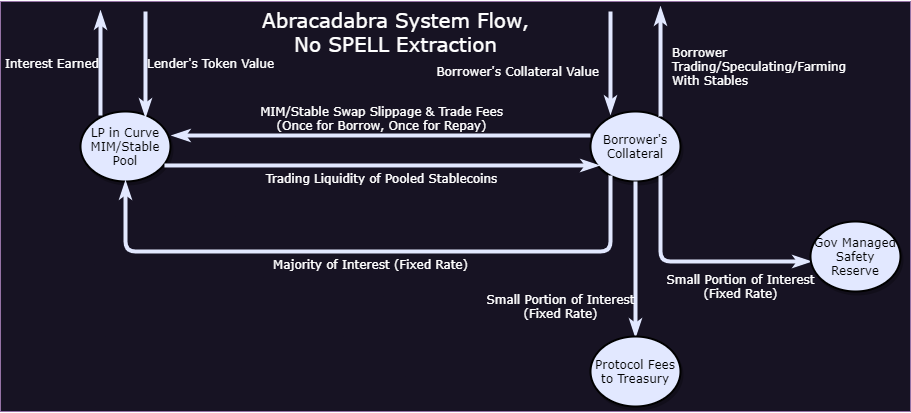

A More Stable and Neutral Incantation

Earlier in our journey we discovered that there were a lot of contingencies and extraction around $SPELL. What would a similar system look like if we cut $SPELL out completely?

Here, we redirected a large majority of the fixed rate interest to incentivizing the MIM-3CRV LPs. At a fair interest rate, this could be enough to incentivize the necessary liquidity to function properly. If some drastic temporary events come along, $MIM may still depeg and incur a sort of temporarily variable interest rate for any borrower that wants to enter/exit their debt positions. These drastic temporary events do also spook the MIM-3CRV LPs, as they start experiencing impermanent loss. If a fixed rate is clearly not longer term sustainable, some governance mechanism (or maybe a slow, delayed feedback loop) could adjust the rate. End result is generally a “fixed” borrow rate that could vary in certain cases for borrowers who want to adjust their positions.

A quick note that this system’s primary flaw is bootstrapping the initial burst of liquidity, which may require some temporary creativity. However, once this initial hurdle is overcome, the system could prove much more stable and sustainable.

Analyzing Other Spellbooks

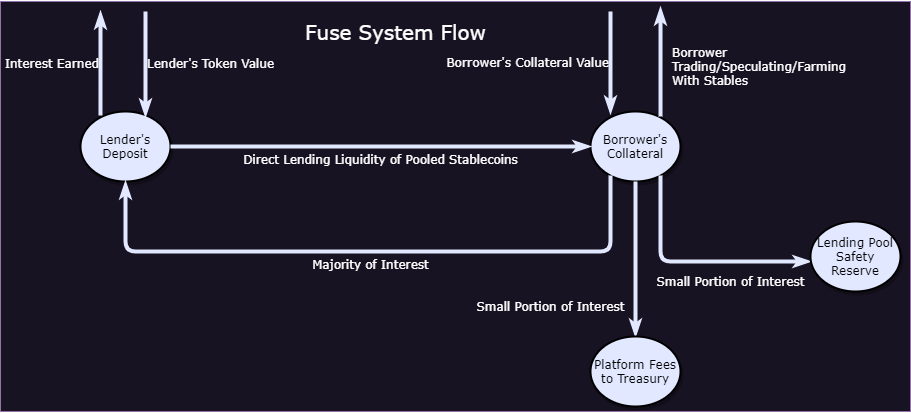

For those with a keen sense of existing DeFi borrowing systems, you may have started to realize that the MIM-3CRV LPs are effectively acting as the lenders (when $MIM isn’t accepted most anywhere), and the combination of the fixed interest rate + $MIM-stablecoin spread from peg is just an interest rate curve of a specific shape. What happens if someone just used a Compound-like money market with their own parameters and tokens?

Funnily enough, that already functionally exists as Fuse within the Rari Capital ecosystem. Anyone can effectively create their own Compound-style money market/lending pool with their own tokens, parameters, interest rate curves, etc! This system minimizes extraction and maximizes efficiency of existing tokens (not creating any new token) by allowing the pool manager to set an appropriate interest rate curve — dynamically reacting exactly as desired. One could build a lending pool that has a fixed interest rate until a utilization % threshold and turn dynamic, while incorporating ibTokens in the pool. Optionally a pool manager could limit risk between assets by controlling which are collateralizable. In fact, a Fuse pool just recently launched containing some ibTokens, and some other pools already have a few sprinkled in.

The hardest part for these lending pools is bootstrapping the first bit of liquidity. After demonstrating that, more liquidity tends to flow in to chase interest rates on certain tokens. Public announcements and also initially self-seeding some liquidity has gone a long way for some of those new lending pools.

Another Disclaimer/Disclosure for Transparency: I am a biased actor when it comes to discussions surrounding Rari Capital, as I have been a supporter for some time and may have a financial stake in Rari Capital’s success. Again, please make sure to do your own research before making any rash decisions. Reread the initial Disclaimer at the top of the page.

Advanced Transfiguration

“Any sufficiently advanced technology is indistinguishable from magic.”

- Arthur C. Clarke

All is not yet lost for Abracadabra & $SPELL. However, major systemic changes towards sustainability would need to happen, and not all solutions have necessarily been discovered/outlined here. From what I have observed, there are two primary reasons why someone would continue to have faith in Abracadabra, $SPELL, and $MIM:

They expect $MIM to become a successfully utilized stablecoin outside of the Abracadabra ecosystem

Especially beneficial if it becomes a ubiquitous stablecoin used throughout DeFi

Very low success rate among existing attempts from other stablecoin projects

They expect the Abracadabra system to be changed into some more sustainable way, where $MIM can remain stable and $SPELL does not subsidize/inflate at a faster rate than it extracts.

Systemic change

Interest rate increase/change

From a personal standpoint, I do think that Abracadabra has a potentially bright future. The devs surrounding it are extremely skilled and well tuned into the desires of the market, so I’m sure they have plenty of tricks up their sleeves. However, there’s certainly some more heavy lifting that needs to be done before the protocol becomes sustainable for all parties involved. In my own opinion, I do think that the borrowing users of the protocol seem like the most-advantaged party as long as there isn’t an exploit. However, I generally anticipate that it will come at the expense of mass $SPELL dilution given the current mechanics.

I’d like to thank you for enduring the long journey — I hope you derived some intellectual value from it. I don’t proclaim to know everything here; I very well could be wrong about a lot of what I shared but still intend to spark a discussion. If you enjoyed this article or have any questions, please contact me to let me know! I look forward to sharing more insights with you on the DeFi galaxy in the future!

Special thanks to all who have read this article in development and provided feedback, including: @DCFgod, @0x_Osprey, @BraveDeFi, @AlphaKetchum, @JHancock, and others!

Technically speaking, if a user wants to deposit into the MIM-3CRV pool they either deposit MIM directly or first acquire the 3CRV LP token by depositing $DAI, $USDC, or $USDT, then deposit directly to receive the MIM-3CRV LP token. This keeps the “standard” stablecoins balanced by accessing the core 3CRV stablecoin pool, which is much more liquid. However, the balance between $MIM and $3CRV still must be maintained.

For now, I’ll assume that the interest in the backfill bucket is used to buy back $SPELL and distribute it in emergency depeg scenarios.

For the sake of this article I’ll assume SPELL buybacks too, although a protocol safety fund should consist of non-native assets.

One cannot argue that $sSPELL holders are providing the service of governance in exchange for more $SPELL. Why? Because there is no direct incentive to do so. If you want this to instead be the case, then use a mechanism to distribute $SPELL exclusively to governance voters. Of course, this does incite further philosophical questions of what the most proper form of voting is and how to build a proper incentives system around it.

While writing this article, a new proposal was recently made that could change that. Also, there is a new SpookySwap incentivized LP. More to come later in the article.

Same point as footnote 5.